Starting a business is a smart move if you’ve got a product or service in high demand. You get to be your own boss, hang onto the profits of your labor and maybe even build an empire.

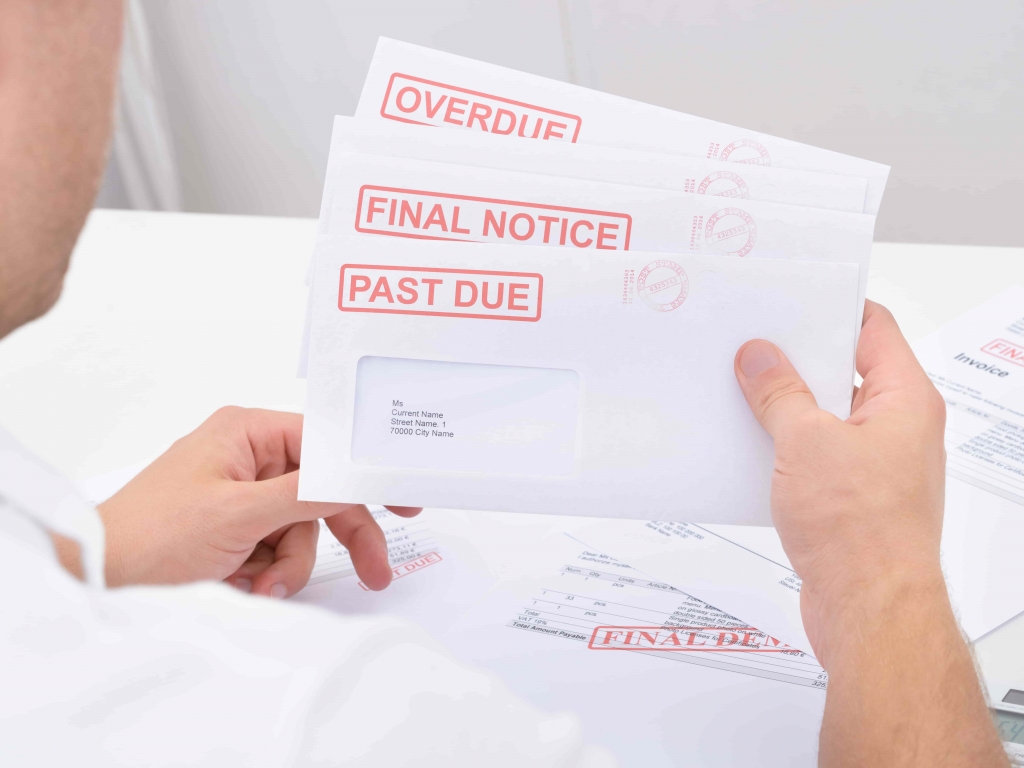

It’s not easy though. Only half of small businesses survive more than five years, according to the Bureau of Labor Statistics. A 50/50 chance of success is quite good considering the potential reward, but it does mean that a lot of businesses find themselves facing obstacles, like financial problems.

It’s likely when you started the business you didn’t have cash on hand, you might have opened a line of credit, used a credit card or even secured a bank loan (if you were able). According to Fundera, 75 percent of new small businesses receive funding through one or more of these methods. However, sooner or later, you’re going to have to pay back the money that you borrowed, often with interest.

For every business owner, there comes a point where you can’t expect to drum up any more business, and you realize your company is in real trouble. What do you do when this happens?

Related: Considerations When Shutting Down Your Business

1. Be Realistic and Take Stock

Realism is essential at this crucial point. Forget about any long shots or Hail Marys. You need to focus on tangible details, such as your cash flow (what money coming in, what is going out) and what assets you currently have at your disposal. The better your understanding of your current situation, the more control you will have over what happens next. Take some time to go through everything in your finances and get a clear picture of where you stand.

Creating a business budget will allow you to do just that and help you avoid incurring any unnecessary debt in the future. Gather all of your bills together and calculate your monthly expenses. Those that are essential to the operation of your business, such as rent, utilities or employee salaries, should be paid first. Next, figure out which bills are important but not immediately essential. Keep going down your line of expenses to figure out which ones you can pay to reduce your total debt faster.

2. Reach Out to Creditors

They may not like to advertise it, but most creditors are willing to work with business owners to help them pay down their debt because they would rather get some money than none at all. Contact your credit card company to see if you can get a lower interest rate. If they agree, more of your monthly payment will go toward your debt principle instead of interest payments, shortening the amount of time it takes for you to close out your loan. If you’re behind on a utility payment, reach out to your provider to see if you qualify for an interest-free payment plan or business-specific account that allows for more lenient payment terms.

Nobody likes to think about the possibility of bankruptcy but, once again, realism is essential here. If your business does reach its conclusion and you are forced to file for bankruptcy, the outcome of proceedings is going to depend very much on how you behaved before bankruptcy. If you made every reasonable effort to settle your debts and treat every creditor equally and fairly, then people will see that you tried to act in good faith. Remember, don’t try to evade your creditors by, for example, signing assets over to family members. Your creditors will track it down – and a judge might find you guilty of fraud.

Not every financial crisis is fatal. In fact, successful business owners will tell you that they had numerous close shaves in their early years. Some may have had failed businesses before they got the formula right. But failure is an opportunity to learn, and those who stay calm and stay professional in difficult times are the ones who succeed in the long run.

3. Cut Spending to the Bone

You can save your business by reducing spending so that it’s less than your income. If your income is a trickle, then your spending needs to get as close to zero as possible. In practice, this means painful decision: cutting staff, not paying yourself, selling equipment, moving from a rented office to your home. Every penny counts right now, so every spending decision needs to be based on absolute necessity. Remember: no matter how hard it is to make cuts, it will be harder to close the business.

Chances are you’re probably spending money on things you don’t necessarily need. Maybe you can operate just as efficiently with three sales people instead of five. Perhaps you can reduce your accounting expenses by switching to an automated software system. It may also be in your interest to try and negotiate a better deal with any suppliers that you have. Paying for goods in advance or switching from a competitor are some of the most common reasons why a supplier might be willing to lower your cost of doing business. The money that you may save by successfully negotiating a new contract could go a long way toward helping you pay down your business debts.

4. Get Additional Help

Even if you are a business veteran, this turbulent time will be stressful and confusing for you. Speak to anyone who might be able to help, from your lawyer and accountant to friends and colleagues with relevant experience. You may also have organizations on hand that can assist.

Consider gaining additional capital to sustain your business for the time being. While most banks will probably not give you a loan in your current state, accounts receivable financing is a great way to use your current customer’s invoices to get cash to pay for your current business needs, like employee wages, rent and your other operations expenses. If you are having a hard time financially, but you know there’s light at the end of the tunnel, this is a great solution for your business.

If you have loans with several different lenders, it may be a good idea to consolidate them under one low-rate loan. A debt consolidation company can help you negotiate the new terms with your lender as well as handle future payment collection. Repaying your loans at a lower interest rate could save you thousands of dollars over the life of your loan. In addition, with less interest to pay down, you’re able to pay off your entire loan in less time. This option works best for business owners with unsecured debt or debt that isn’t backed by collateral or company assets.

5. Collect on Debts

One of the biggest problems for small business is non-payment of invoices. Even reputable clients can sometimes have punitive payment cycles that force you to wait for months before invoices are settled. If your business is on the line, however, you need to get tough. Push your debtors to settle their account according to the payment terms set by you – not them. Small businesses are often reluctant to take this approach for fear of losing future business, but if your company is on the line then you don’t have a choice.

Further Considerations When Downsizing

For any business owner, facing the decision to downsize, close or pivot spending can be stressful, not to mention, confusing. You can never be too sure about shutting down the new location you have invested in so much or selling that new equipment. However, certain events taking into account certain can help with easier decision-making when trying to look to the future of your business. Consider these situations when making these dire decisions with your company:

An Economic Downturn

The nature of the modern capitalistic economy is characterized by a constant ebb and flow. However, in a 2008-like financial crisis, it would be wiser to downsize than to continue burning cash. A good way to tell the magnitude of a downturn is to look at the big players in your industry. If they are having prolonged cash flow issues as well you need to consider downsizing.

Reduced Profitability

If your profits have been decreasing for more than three quarters consecutively, consider cutting back on some of your services.

It is important to figure out the cause of decreased profits. If increased overhead is the primary cause, downsizing may be a wise choice. However, if a declining customer base is behind it, investing in new marketing strategies could be a better strategy.

Difficulty Maintaining Service Standards

If you find that your projects are constantly running behind schedule ever since you added a new service, perhaps you need to reconsider the additional workload this has created. If your staff are unable to meet demand, but you are compelled to offer the service to remain competitive, you could outsource it temporarily.

Failure to meet project deadlines repeatedly, or a rise in consumer complaints are telltale signs that you need to reduce the number of services you offer in order to maintain service standards. Once you have redistributed the workload and your staff is ready for the new challenge, you can bring it back in-house.

Alternatives to Downsizing

Before you downsize, consider other options that can ease the financial distress.

Factoring

Weak cash flow is one of the most common reasons for small businesses to fail. Fortunately, it can be solved with the help of factoring, especially if you are in the Business to Business services. Factoring involves selling your outstanding invoices to a financing company. You receive the majority of the funds owed up front, while the factor takes on collecting the full amount from your client. Factoring is a better option than taking a loan because you do not have to pay back the funds and you receive quick access to the capital you need.

Small Business Loan

If your financial situation extends beyond cash flow issues, you may consider taking a small loan. However, ensure you have analyzed your cash flow and profit projections before you take on additional debt. You should be certain of terms and repayment ability before you apply for a business loan. Be prepared to meet with a loan officer and discuss the strength and profitability of your business.

The decision to downsize your business either through services or locations is a very difficult one, not to be made lightly. Give deep consideration to all options before moving forward with any plans. You have choices to make which will impact your business for years to come. Be sure your long-term goals and legacy are reflected in these choices.